Realtor.com’s new 2025 Home Trends Report found that efficiency, sustainability and nature-inspired design are on the rise, while more opulent or space-heavy features are losing ground—highlighting a shift in how Americans define comfort and value. Sustainability and Efficiency There is a pronounced shift toward sustainable, eco-friendly home design in 2025, driven largely by increasing awareness [...]

Construction + Economy

Commercial Construction Surges 11.9% In September MoM

The September 2025 Dodge Construction Network data show a continued rebound in total construction starts, with a 3.1% month-over-month increase to a seasonally adjusted annual rate (SAAR) of about $1.26 trillion. The upturn is driven primarily by a sharp rise in nonresidential starts, which climbed 11.9% for the month, while residential starts rose 3.6%. [...]

Construction + Economy, Sustainability

A Surge In Apartment Conversion Projects

Apartment conversion projects surged across the U.S. in 2024, characterized by both the volume and pace of adaptive reuse—where underperforming properties are redeveloped into multifamily residential units. According to a new RentCafe report, nearly 25,000 apartments were completed through adaptive reuse in 2024, representing a 50% increase compared to 2023 and double 2022’s output. [...]

Construction + Economy, Lighting Industry

CMG Q3 2025 Pulse Of Lighting Reports Stagnant Market

The 2025 Q3 Pulse of the Lighting Market report is produced by Channel Marketing Group with William Blair. The Q3 2025 report finds that the U.S. lighting industry faced a challenging, largely stagnant quarter, with most companies experiencing low or no growth, even after factoring in price increases driven by new tariffs. Increased prices [...]

Construction + Economy, Lighting Industry

US-China Trade War Gets Extreme: Everyone Looses

On Friday, the United States and China reignited their trade war in dramatic fashion, raising significant concerns about near-term economic volatility and long-term global implications. After months of relative calm, President Donald Trump announced the imposition of sweeping 100% tariffs on all Chinese imports, effective November 1, in retaliation for China’s newly tightened export [...]

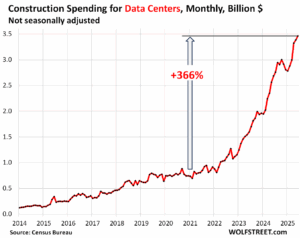

Data Center Construction Spending Soars

Data centers have rapidly reshaped the landscape of U.S. office construction, now representing a major share of spending and signaling a long-term shift in commercial real estate investment priorities. As of 2024, data centers accounted for 32% of new office construction spending in the U.S., a dramatic increase from just 5% a decade ago. [...]

Construction + Economy, Lighting Industry

What To Know About The “Blended Workforce”

Traditional employment models are transforming into a dynamic, flexible system now known as the blended workforce. This evolution challenges old norms, such as long-term, full-time employment at a single company and offices filled exclusively with permanent staff, by integrating a variety of talent sources and technological advancements. A blended workforce is defined by the [...]

Warehouse Real Estate Declines After 15 Years Of Growth

Demand for U.S. industrial space—especially in the warehouse sector—fell for the first time in fifteen years during the second quarter of 2025, signaling a dramatic shift in commercial real estate dynamics since the pandemic-era boom. This decline was marked by an 11.3 million square foot contraction in the second quarter alone, with total net [...]

Construction + Economy, Lighting Industry

Single Family Construction Down, Multifamily Up

Recent trends in U.S. housing construction highlight how single-family housing starts have declined while multifamily construction has grown—primarily in smaller and less densely populated markets—during the second quarter of 2025, according to the NAHB Home Building Geography Index (HBGI). Single-Family Construction Declines Single-family construction experienced declines in nearly every region during Q2 2025, signaling [...]

Construction + Economy, Lighting Industry

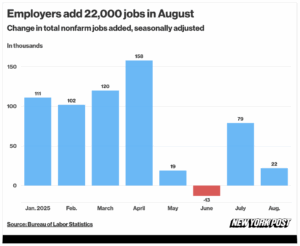

Recession Concerns Increase As Job Growth Slows

The risk of a recession in September 2025 is elevated, with analysts citing a combination of slow job growth, persistent inflation, and rising tariffs as key factors pushing the U.S. economy toward a downturn. Some, like Moody’s Chief Economist Mark Zandi, suggest the U.S. is “on the precipice” of a downturn, with the period of greatest [...]

Lighting Solution Development

7889 River Hill Lane, Alexandria, PA 16611-2604